ATSAUCĒ IETVERT:

International Convention on the simplification and harmonization of Customs procedures. Publicēts oficiālajā laikrakstā "Latvijas Vēstnesis", 28.10.1998., Nr. 317/320 https://www.vestnesis.lv/ta/id/218774

|

RĪKI

Publikācijas atsauceATSAUCĒ IETVERT:

International Convention on the simplification and harmonization of Customs procedures. Publicēts oficiālajā laikrakstā "Latvijas Vēstnesis", 28.10.1998., Nr. 317/320 https://www.vestnesis.lv/ta/id/218774

Paraksts pārbaudītsNĀKAMAIS Latvijas Republikas valdības un Baltkrievijas Republikas valdības līgums par savstarpējo palīdzību muitas jautājumos Vēl šajā numurā28.10.1998., Nr. 317/320 |

PAR DOKUMENTU Veids: starptautisks dokuments Pieņemts: 18.05.1973. |

PREAMBLE

The CONTRACTING PARTIES to the present Convention, established under the auspices of the Customs Co-operation Council,

Noting that divergences between national Customs procedures can hamper international trade and other international exchanges,

Considering that it is in the interests of all countries to promote such trade and exchanges and to foster international co-operation,

Considering that simplification and harmonization of their Customs procedures can effectively contribute to the development of international trade and of other international exchanges,

Convinced that an international instrument proposing provisions which countries undertake to apply as soon as they are able to do so would lead progressively to a high degree of simplification and harmonization of Customs procedures, which is one of the essential aims of the Customs Co-operation Council,

Have agreed as follows:

Chapter I

Definitions

Article 1

For the purposes of this Convention:

(a) the term "the Council" means the Organization set up by the Convention establishing a Customs Co-operation Council, done at Brussels on 15 December 1950;

(b) the term "Permanent Technical Committee" means the Permanent Technical Committee of the Council;

(c) the term "ratification" means ratification, acceptance or approval.

Chapter II

Scope of the Convention and structure of the Annexes

Article 2

Each Contracting Party undertakes to promote the simplification and harmonization of Customs procedures and, to that end, to conform, in accordance with the provisions of this Convention, to the Standards and Recommended Practices in the Annexes to this Convention. However, nothing shall prevent a Contracting Party from granting facilities greater than those provided for therein, and each Contracting Party is recommended to grant such greater facilities as extensively as possible.

Article 3

The provisions of this Convention shall not preclude the application of prohibitions or restrictions imposed under national legislation.

Article 4

Each Annex to this Convention consists in principle, of:

(a) an introduction summarizing the various matters dealt with in the Annex;

(b) definitions of the main Customs terms used in the Annex;

(c) Standards, being those provisions the general application of which is recognized as necessary for the achievement of harmonization and simplification of Customs procedures;

(d) Recommended Practices, being those provisions which are recognized as constituting progress towards the harmonization and the simplification of Customs procedures, the widest possible application of which is considered to be desirable;

(e) Notes, indicating some of the possible courses of action to be followed in applying the Standard or Recommended Practice concerned.

Article 5

1. Any Contracting Party which accepts an Annex shall be deemed to accept all the Standards and Recommended Practices therein unless at the time of accepting the Annex or at any time thereafter it notifies the Secretary General of the Council of the Standard(s) and Recommended Practice(s) in respect of which it enters reservations, stating the differences existing between the provisions of its national legislation and those of the Standard(s) and Recommended Practice(s) concerned. Any Contracting Party which has entered reservations may withdraw them, in whole or in part, at any time, by notification to the Secretary General specifying the date on which such withdrawal takes effect.

2. Each Contracting Party bound by an Annex shall at least once every three years review the Standards and Recommended Practices therein in respect of which it has entered reservations, compare them with the provisions of its national legislation and notify the Secretary General of the Council of the results of that review.

Chapter III

Role of the Council and of the Permanent Technical Committee

Article 6

1. The Council shall, in accordance with the provisions of this Convention, supervise the administration and development of this Convention. It shall, in particular, decide upon the incorporation of new Annexes in the Convention.

2. To these ends the Permanent Technical Committee shall, under the authority of the Council, and in accordance with any directions given by the Council, have the following functions:

(a) to prepare new Annexes and to propose to the Council their adoption with a view to their incorporation in the Convention;

(b) to submit to the Council proposals for such amendments to this Convention or to its Annexes as it may consider necessary and, in particular, proposals for amendments to the texts of the Standards and Recommended Practices and for the upgrading of Recommended Practices to Standards;

(c) to furnish opinions on any matters concerning the application of the Convention;

(d) to perform such tasks as the Council may direct in relation to the provisions of the Convention.

For the purposes of voting in the Council and in the Permanent Technical Committee each Annex shall be taken to be a separate convention.

Article 7

For the purposes of voting in the Council and in the Permanent Technical Committee each Annex shall be taken to be a separate convention.

Chapter IV

Miscellaneous provisions

Article 8

For the purposes of this Convention, any Annex or Annexes to which a Contracting Party is bound shall be construed to be an integral part of the Convention, and in relation to that Contracting Party any reference to the Convention shall be deemed to include a reference to such Annex or Annexes.

Article 9

Contracting Parties which form a Customs or Economic Union may state by notification to the Secretary General of the Council that for the application of a given Annex to this Convention their territories are to be taken as a single territory. In each instance where, as a result of such notification differences exist between the provisions of that Annex and those of the legislation applicable to the territories of the Contracting Parties, the States concerned shall enter a reservation to the Standard or Recommended Practice in question under Article 5 of the Convention.

Chapter V

Final provisions

Article 10

1. Any dispute between two or more Contracting Parties concerning the interpretation or application of this Convention shall so far as possible be settled by negotiation between them.

2. Any dispute which is not settled by negotiation shall be referred by the Contracting Parties in dispute to the Permanent Technical Committee which shall thereupon consider the dispute and make recommendations for its settlement.

3. If the Permanent Technical Committee is unable to settle the dispute, it shall refer the matter to the Council which shall make recommendations in conformity with Article III(e) of the Convention establishing the Council.

4. The Contracting Parties in dispute may agree in advance to accept the recommendations of the Permanent Technical Committee or Council as binding.

Article 11

1. Any State Member of the Council and any State Member of the United Nations or its specialized agencies may become a Contracting Party to this Convention:

(a) by signing it without reservation of ratification;

(b) by depositing an instrument of ratification after signing it subject to ratification; or

(c) by acceding to it.

2. This Convention shall be open until 30th June 1974 for signature at the Headquarters of the Council in Brussels by the States referred to in paragraph 1 of this Article. Thereafter, it shall be open for their accession.

3. Any State, not being a Member of the Organizations referred to in paragraph 1 of this Article, to which an invitation to that effect has been addressed by the Secretary General of the Council at the Council's request, may become a Contracting Party to this Convention by acceding thereto after its entry into force.

4. Each State referred to in paragraph 1 or 3 of this Article shall at the time of signing ratifying or acceding to this Convention specify the Annex or Annexes it accepts, it being necessary to accept at least one Annex. It may subsequently notify the Secretary General of the Council that it accepts one or more further Annexes.

5. The instruments of ratification or accession shall be deposited with the Secretary General of the Council.

6. The Secretary General of the Council shall notify the Contracting Parties to this Convention, the other signatory States, those States Members of the Council that are not Contracting Parties to the Convention, and the Secretary General of the United Nations of any new Annex that the Council may decide to incorporate in this Convention. Contracting Parties accepting such a new Annex shall notify the Secretary General of the Council in accordance with paragraph 4 of this Article.

7. The provisions of paragraph 1 of this Article shall also apply to the Customs and Economic Unions referred to in Article 9 of this Convention in so far as the obligations arising from the instruments establishing such Customs or Economic Unions require the competent bodies thereof to contract in their own name. However, such bodies shall not have the right to vote.

Article 12

1. This Convention shall enter into force three months after five of the States referred to in paragraph 1 of Article 11 thereof have signed the Convention without reservation of ratification or have deposited their instruments of ratification or accession.

2. For any State signing without reservation of ratification, ratifying or acceding to this Convention after five States have signed it without reservation of ratification or have deposited their instruments of ratification or accession, this Convention shall enter into force three months after the said State has signed without reservation of ratification or deposited its instrument of ratification or accession.

3. Any Annex to this Convention shall enter into force three months after five Contracting Parties have accepted that Annex.

4. For any State which accepts an Annex after five States have accepted it, that Annex shall enter into force three months after the said State has notified its acceptance.

Article 13

1. Any State may, at the time of signing this Convention without reservation of ratification or of depositing its instrument of ratification or accession, or at any time thereafter, declare by notification given to the Secretary General of the Council that this Convention shall extend to all or any of the territories for whose international relations it is responsible. Such notification shall take effect three months after the date of the receipt thereof by the Secretary General of the Council. However, the Convention shall not apply to the territories named in the notification before the Convention has entered into force for the State concerned.

2. Any State which has made a notification under paragraph 1 of this Article extending this Convention to any territory for whose international relations it is responsible may notify the Secretary General of the Council, under the procedure of Article 14 of this Convention, that the territory in question will no longer apply the Convention.

Article 14

1. This Convention is of unlimited duration but any Contracting Party may denounce it at any time after the date of its entry into force under Article 12 thereof.

2. The denunciation shall be notified by an instrument in writing deposited with the Secretary General of tie Council.

3. The denunciation shall take effect six months after the receipt of the instrument of denunciation by the Secretary General of the Council.

4. The provisions of paragraphs 2 and 3 of this Article shall also apply in respect of the Annexes to this Convention, any Contracting Party being entitled, at any time after the date of their entry into force under Article 12 of the Convention, to withdraw its acceptance of one or more Annexes. Any Contracting Party which withdraws its acceptance of all the Annexes shall be deemed to have denounced the Convention.

Article 15

1. The Council may recommend amendments to this Convention. Every Contracting Party shall be invited by the Secretary General of the Council to participate in the discussion of proposals for amendment of this Convention.

2. The text of any amendment so recommended shall be communicated by the Secretary General of the Council to all Contracting Parties to this Convention, to the other signatory States and to those States Members of the Council that are not Contracting Parties to this Convention.

3. Within a period of six months from the date on which the recommended amendment is so communicated, any Contracting Party or, if the amendment affects an Annex in force, any Contracting Party bound by that Annex, may inform the Secretary General of the Council:

(a) that it has an objection to the recommended amendment, or

(b) that, although it intends to accept the recommended amendment, the conditions necessary for such acceptance are not yet fulfilled in its country.

4. If a Contracting Party sends the Secretary General of the Council a communication as provided for in paragraph 3 (b) of this Article, it may, so long as it has not notified the Secretary General of its acceptance of the recommended amendment, submit an objection to that amendment within a period of nine months following the expiry of the six-month period referred to in paragraph 3 of this Article.

5. If an objection to the recommended amendment is stated in accordance with the terms of paragraph 3 or 4 of this Article the amendment shall be deemed not to have been accepted and shall be of no effect.

6. If no objection to the recommended amendment in accordance with paragraph 3 or 4 of this Article has been stated, the amendment shall be deemed to have been accepted as from the date specified below:

(a) if no Contracting Party has sent a communication in accordance with paragraph 3 (b) of this Article, on the expiry of the period of six months referred to in paragraph 3;

(b) if any Contracting Party has sent a communication in accordance with paragraph 3 (b) of this Article, on the earlier of the following two dates:

(i) the date by which all the Contracting Parties which sent such communications have notified the Secretary General of the Council of their acceptance of the recommended amendment, provided that, if all the acceptances were notified before the expiry of the period of six months referred to in paragraph 3 of this Article, that date shall be taken to be the date of expiry of the said six-month period;

(ii) the date of expiry of the nine-month period referred to in paragraph 4 of this Article.

7. Any amendment deemed to be accepted shall enter into force either six months after the date on which it was deemed to be accepted or, if a different period is specified in the recommended amendment, on the expiry of that period after the date on which the amendment was deemed to be accepted.

8. The Secretary General of the Council shall, as soon as possible, notify the Contracting Parties to this Convention and other signatory States of any objection to the recommended amendment made in accordance with paragraph 3 (a), and of any communication received in accordance with paragraph 3 (b), of this Article. He shall subsequently inform the Contracting Parties and other signatory States whether the Contracting Party or Parties which have sent such a communication raise an objection to the recommended amendment or accept it.

Article 16

1. Independently of the amendment procedure laid down in Article 15 of this Convention any Annex, excluding its definitions, may be modified by a decision of the Council. Every Contracting Party to this Convention shall be invited by the Secretary General of the Council to participate in the discussion of any proposal for the amendment of an Annex. The text of any amendment so decided upon shall be communicated by the Secretary General of the Council to the Contracting Parties to this Convention, the other signatory States and those States Members of the Council that are not Contracting Parties to this Convention.

2. Amendments decided upon under paragraph 1 of this Article shall enter into force six months after their communication by the Secretary General of the Council. Each Contracting Party bound by an Annex forming the subject of such amendments shall be deemed to have accepted those amendments unless it enters a reservation under the procedure of Article 5 of this Convention.

Article 17

1. Any State ratifying or acceding to this Convention shall be deemed to have accepted .any amendments thereto which have entered into force at the date of deposit of its instrument of ratification or accession.

2. Any State which accepts an Annex shall be deemed, unless it enters reservations under Article S of this Convention, to have accepted 311y amendments to that Annex which have entered into force at the date on which it notifies its acceptance to the Secretary General of the Council.

Article 18

The Secretary General of the Council shall notify the Contracting Parties to this Convention, the other signatory States, those States Members of the Council that are not Contracting Parties to this Convention, and the Secretary General of the United Nations of:

(a) signatures, ratifications and accessions under Article 11 of this Convention;

(b) the date of entry into force of this Convention and of each of the Annexes in accordance with Article 12;

(c) notifications received in accordance with Articles 9 and 13;

(d) notifications and communications received in accordance with Articles 5, 16 and 17;

(e) denunciations under Article 14;

(f) any amendment deemed to have been accepted in accordance with Article 15 and the date of its entry into force;

(g) any amendment to the Annexes adopted by the Council in accordance with Article 16 and the date of its entry into force.

Article 19

In accordance with Article 102 of the Charter of the United Nations, this Convention shall be registered with the Secretariat of the United Nations at the request of the Secretary General of the Council.

In witness whereof the undersigned, being duly authorized thereto, have signed this Convention.

Done at Kioto, this eighteenth day of May nineteen hundred and seventy-three, in the English and French languages, both texts being equally authentic, in a single original which shall be deposited with the Secretary General of the Council who shall transmit certified copies to all the States referred to in paragraph 1 of Article 11 of this Convention.

Introduction

Goods may be introduced into a country by many different modes of transport. In order to safeguard the Revenue and ensure compliance with national legislation, the carrier having introduced goods into the Customs territory must produce them, and the means of transport by which they are carried, to the Customs authorities at the earliest possible time. The provisions necessary to control the introduction of goods into the Customs territory depend, to a large extent, upon the geography of the country and other circumstances such as the principal modes of transport bringing goods into the country.

In many cases the Customs office at which the goods are to be produced and the Goods declaration is to be lodged is situated at the place where the goods are introduced into the Customs territory; however, in other cases, this Customs office is situated some distance from that place. It is essential that the Customs authorities be in a position to Control the conveyance of goods to the Customs office at which the goods are to be produced to the Customs.

The interests of the Customs may be safeguarded by placing obligations on the carrier through regulations and by means of physical surveillance by the Customs of means of transport and goods introduced into the Customs territory.

It is important that these measures cause a minimum of inconvenience to international trade. To this end all formalities to be accomplished by the carrier should be as simple as possible and information concerning them should be readily available to all interested persons.

This Annex does not cover goods which arrive under a Customs procedure, e.g. international Customs transit, goods carried by post or in travellers' baggage or the temporary storage of goods; nor does it cover certain other formalities which may be applicable in the case of particular modes of transport, e.g. presentation of a report on the arrival of a ship.

Definitions

For the purposes of this Annex:

(a) the term "Customs formalities prior to the lodgement of the Goods declaration" means all the operations to be carried out by the person concerned and by the Customs from the time goods are introduced into the Customs territory to the placing of the goods under a Customs procedure;

Note

Temporary storage may be considered as a Customs procedure.

(b) the term "Customs territor" means the territory in which the Customs law of a State applies in full;

(c) the term "carrie" means the person actually transporting goods or in charge of or responsible for the operation of the means of transport;

(d) the term "import duties and taxe" means Customs duties and all other duties, taxes, fees or other charges which are collected on or in connexion with the importation of goods, but not including fees and charges which are limited in amount to the approximate cost of services rendered;

(e) the term "Goods declaratio" means a statement made in the form prescribed by the Customs, by which the persons interested indicate the particular Customs procedure to be applied to the goods and furnish the particulars which the Customs require to be declared for the application of that procedure;

(f) the term "Customs contro" means measures applied to ensure compliance with the laws and regulations which the Customs are responsible for enforcing;

(g) the term "person" means both natural and legal persons unless the context otherwise requires.

Principles

1. Standard

Customs formalities prior to the lodgement of the Goods declaration shall be governed by the provisions of this Annex.

2. Standard

National legislation shall specify the conditions to be fulfilled and the formalities to be accomplished in respect of goods which are introduced into the Customs territory.

3. Standard

All goods which are introduced into the Customs territory, regardless of whether they are liable to import duties and taxes, shall be subject to Customs control.

4. Standard

Customs formalities prior to the lodgement of the Goods declaration shall be reduced to the minimum necessary to ensure compliance with the laws and regulations which the Customs are responsible for enforcing.

5. Standard

Customs formalities prior to the lodgement of the Goods declaration shall apply equally, regardless of the country of origin of the goods or the country whence they arrived.

Introduction of goods into the Customs territory

Places at Which goods may be introduced into the Customs territory

6. Standard

National legislation shall specify the places at which goods may be introduced into the Customs territory. In determining these places the factors to be taken into account shall include the particular requirements of trade, industry and transport.

Note

Countries may specify for this purpose the Customs routes, that is to say, the roads, railways, waterways and any other routes (pipelines, etc.) which must be used for the importation of goods.

Obligations of the carrier

7. Standard

The fact of having introduced goods into the Customs territory shall carry with it the obligation upon the carrier to convey them directly to a designated Customs office or other place specified by the Customs authorities without altering their nature or their packaging.

8. Standard

Where the conveyance of the goods from the place of their introduction into the Customs territory to a designated Customs office or other specified place is interrupted by accident or force majeure the carrier shall be required to take precautions to prevent the goods from entering into unauthorized circulation and to advise the Customs or other competent authorities of the nature of the accident or other circumstance which has interrupted the journey.

Customs control

9. Standard

Customs control in respect of imported goods shall be reduced to the minimum.

Notes

1. Customs control may include the boarding and searching of means of transport.

2. The Customs authorities may have the power to take special control measures which are applied only in specified areas, for example, in the frontier zone.

3. As a rule it is not necessary to take control measures which involve unloading goods, affixing seals or identification marks to means of transport or goods or conveyance of goods under Customs escort. However where the Customs authorities consider such control measures to be indispensable, they would apply those which would cause the least inconvenience to both the Customs and the carrier while still providing adequate safeguards. Customs seals and identification marks affixed by foreign Customs authorities would normally be accepted unless they were considered not to be sufficient or secure.

Production of goods to the Customs

Documentation

10. Recommended Practice

Where the Customs office at which the goods are to be produced is not located at the place where the goods are introduced into the Customs territory no document should be required to be lodged with the Customs authorities at that place.

Note

For the purpose of identifying the goods the Customs authorities may require the presentation of commercial, transport or other accompanying documents.

11. Standard

Where the Customs authorities require documentation in respect of the production of the goods to the Customs this shall not be required to contain more than the information necessary to identify the goods and the means of transport.

Note

The information is normally obtained from commercial and transport documents the contents of which may vary from one mode of transport to another. The Customs authorities would not normally require any more than a description of the goods and of the packages (marks and numbers, number and kind, weight) and identification of the means of transport. Some international agreements lay down the maximum information which may be required (e.g. the country may be a Contracting Party to Annex 9 to the Convention on International Civil Aviation or the Convention on Facilitation of International Maritime Traffic).

12. Recommended Practice

Where the documents produced to the Customs are made out in a language which is not specified for this purpose or in a language which is not a language of the country into which the goods are introduced a translation of the particulars given in those documents should not be required as a matter of course.

Competence and homers of business of Customs offices

13. Standard

The Customs authorities shall designate the Customs offices at which goods may be produced to the Customs. In determining the competence of these offices and their hours of business, the factors to be taken into account shall include the particular requirements of trade and industry and transport. I

Notes

1. In some countries the competence of the Customs offices is determined with reference to the Customs routes and their importance.

2. Where necessary the competence of certain Customs offices may be restricted to certain modes of transport or to certain categories of goods or to goods consigned to specified areas (e.g. the frontier zone or an industrial zone).

14. Recommended Practice

Where corresponding Customs offices are located on a common frontier, the Customs authorities of the two countries concerned should correlate the business hours and the competence of those offices.

Note

In some cases joint controls have been established at common frontiers with Customs offices of the two countries installed at the same place and sometimes in the same building.

Arrival outside wording hours

15. Standard

The Customs authorities shall specify the precautions to be taken by the carrier to prevent the goods from entering into unauthorized circulation in the Customs territory when they arrive at a Customs office outside working hours.

Note

The carrier may be required to keep the goods at a specific place at or in the vicinity of the Customs office.

16. Recommended Practice

At the request of the carrier, and for reasons deemed valid by the Customs authorities, the latter should, so far as possible allow the Customs formalities prior to the lodgement of the Goods declaration to be accomplished outs de the business hours of the Customs office; any expenses which this entails may he charged to the carrier.

Unloading

Places of unloading

17. Standard

National legislation shall specify the places which are approved for unloading.

18. Recommended Practice

At the request of the person concerned, and for reasons deemed valid by the Customs authorities, the latter should allow goods to be unloaded at a place other than the one approved for unloading; any expenses which this entails may be charged to the person concerned.

Note

Goods may be unloaded, according to the circumstances, at the premises of the person concerned, at premises with appropriate equipment or at any place within the Customs surveillance zone.

Commencement of unloading

19. Recommended Practice

The commencement of unloading should be permitted as soon as possible after the arrival of the means of transport at the place of unloading.

20. Recommended Practice

At the request of the person concerned and for reasons deemed valid by the Customs authorities, the latter should, so far as administrative circumstances permit, allow unloading to proceed outside the business hours of the Customs office; any expenses which this entails may he charged to the person concerned.

Goods damaged, destroyed or lost

21. Standard

Total or partial exemption, as the case may be, from payment of import duties and

taxes shall be granted in respect of goods damaged, destroyed or irrecoverably lost by accident or force majeure during the accomplishment of the Customs formalities prior to the lodgement of the Goods declaration provided that the facts are duly established to the satisfaction of the Customs authorities.

Note

At the request of the person concerned remnants of goods covered by this Standard may be:

(a) cleared for home use in their existing state as if they had been imported in that state; or

(b) re-exported; or

(c) rendered commercially valueless under Customs control, without expense to the Revenue; or

(d) with the consent of the Customs authorities, abandoned free of all expenses to the Revenue.

Responsibility for the payment of import duties and taxes

22. Standard

National legislation shall specify the person or persons responsible for the payment of any import duties and taxes in respect of goods introduced into the Customs territory which have not been produced to the Customs in compliance with the conditions and formalities to be fulfilled prior to the lodgement of the Goods declaration.

Information concerning customs formalities prior to the lodgement of the Goods declaration

23. Standard

The Customs authorities shall ensure that all relevant information regarding Customs formalities prior to the lodgement of the Goods declaration is readily available to any person interested.

Introduction

It is important that, on arrival, goods may be permitted to be unloaded from the means of transport as soon as possible. In recognition of this fact Customs administrations have introduced arrangements under which the discharge of cargo may commence as soon as possible after arrival with a minimum of formalities subject to the Revenue being safeguarded.

For a variety of reasons some time may elapse between the arrival of the goods and the lodgement of the relevant Goods declaration. In these circumstances Customs authorities require the goods to be kept under Customs control and for this purpose they are usually placed in a specified area where they are stored pending lodgement of the Goods declaration. Such areas are termed temporary stores and may consist of buildings or may be enclosed or unenclosed spaces.

The provisions of this Annex do not apply to the storage of goods in Customs warehouses or in free zones.

Definitions

For the purposes of this Annex:

(a) the term "temporary storage of goods" means the storing of goods under Customs control in premises and enclosed or unenclosed spaces specified by the Customs (hereinafter called temporary stores) pending lodgement of the Goods declaration;

(b) the term "import duties and taxes" means Customs duties and all other duties, taxes, fees or other charges which are collected on or in connexion with the importation of goods, but not including fees and charges which are limited in amount to the approximate cost of services rendered;

(c) the term "Goods declaration" means a statement made in the form prescribed by the Customs, by which the persons interested indicate the Customs procedure to be applied to the goods and furnish the particulars which the Customs require to be declared for the application of that procedure;

(d) the term "Customs control" means measures applied to ensure compliance with the laws and regulations which the Customs are responsible for enforcing;

(e) the term "security" means that which ensures to the satisfaction of the Customs that an obligation to the Customs will be fulfilled. Security is described as " general " when it ensures that the obligations arising from several operations will be fulfilled;

(f) the term "person" means both natural and legal persons, unless the context otherwise requires.

Principles

1. Standard

The temporary storage of goods shall be governed by the provisions of this Annex.

2. Standard

National legislation shall specify the conditions to be fulfilled and the formalities to be accomplished in respect of goods placed in temporary store.

Scope

3. Standard

The Customs authorities shall authorize the establishment of temporary stores when ever they deem it necessary to mcet the requirements of trade and industry.

Notes

1. In accordance with the provisions of n.ltiollal legislation, temporary stores may be Inallaged by the Customs authorities, by other authorities or by natural or legal persons.

2. Temporary stores may be open to all importers and other persons entitled to dispose of goods being imported, or use of them may be restricted to specified persons.

4. Standard

Temporary storage shall be allowed in respect of all kinds of goods irrespective of quantity, country of origin or country whence arrived. However, goods which constitute a hazard, which are likely to affect other goods or which require special installations shall be admitted only into temporary stores specially designed to receive them.

5. Standard

The only document to be required when goods are placed in temporary store shall be that used to describe the goods when they are produced to the Customs.

Management of temporary stores

6. Standard

The requirements as regards the construction, layout and management of temporary stores and the arrangements for the storage of goods, for stock-keeping and accounting and for Customs control shall be laid down by the Customs authorities.

Notes

1. For the purposes of control the Customs may, in particular:

— keep, or require to be kept, accounts of goods placed in the temporary store (by using either special registers or the relevant documentation):

— keep the temporary store under permanent or intermittent supervision;

— require that the temporary store be double-locked (secured by the lock of the person concerned and by Customs lock);

— take stock of the goods in the temporary store from time to time.

2. Goods are usually required to be stored in locked premises. However, bulky or heavy goods and low-duty goods which constitute little Revenue risk are frequently stored in unenclosed spaces under Customs supervision.

7. Standard

National legislation shall specify the person or persons held responsible for the payment of any import duties and taxes chargeable on goods placed in a temporary store which are not accounted for to the satisfaction of the Customs authorities.

8. Standard

When security is required from the authority or person managing a temporary store, the Customs authorities shall accept a general security.

9. Recommended Practice

The amount of any security should be set as low as possible having regard to the import duties and taxes potentially charge able.

10. Recommended Practice

The Customs authorities should waive security where the temporary store is under adequate Customs supervision, in particular where it is Customs locked.

Authorized operations

11. Standard

Any person entitled to dispose of goods in temporary stores shall, for the purposes of preparing the Goods declaration, be allowed to:

(a) inspect them;

(b) weigh them;

(c) take samples, against payment of the import duties and taxes where appropriate.

12. Standard

Goods in temporary store shall be allowed to undergo normal operations necessary for their preservation in their unaltered state.

Note

The normal operations necessary for the preservation of the goods in their unaltered state may include cleaning, beating, removal of dust, sorting and repair or change of faulty packings.

13. Recommended Practice

Goods in temporary store should be allowed under such conditions as may be laid down by the Customs authorities, to undergo normal operations necessary to facilitate their removal from store and their further transport.

Note

These operations may include sorting piling, weighing, marking, labelling. They may also involve the consolidation of different consignments of goods intended for further transport under a single transport document and/or a single Customs document (groupage).

Duration of temporary storms

14. Standard

Where national legislation lays down a time limit for temporary storage, the time allowed shall be sufficient to enable the importer to complete the necessary formalities to place the goods under a Customs procedure.

Note

The time limit laid down may vary according to the mode of transport used, and in the case of goods imported by sea may well be of considerable duration.

15. Recommended Practice

At the request of the person concerned and for reasons deemed valid by the Customs authorities, the latter should extend the period initially fixed.

Deterioration, damage, loss, destruction or abandonment of goods

16. Standard

Goods deteriorated, spoiled or damaged by accident or force majeure before leaving the temporary store shall be allowed to be cleared as if they had been imported in their deteriorated, spoiled or damaged state.

17. Standard

Goods in temporary store which are destroyed or irrecoverably lost by accident or force majeure shall not be subjected to import duties and taxes, provided that such destruction or loss is duly established to the satisfaction of the Customs authorities.

Any waste or scrap remaining after destruction shall be liable, if taken into home use, to the import duties and taxes that would be applicable to such waste and scrap imported in that state.

18. Standard

At the request of the person entitled to dispose of them, goods in temporary store shall be allowed to be abandoned, in whole or in part, to the Revenue or to be destroyed or rendered commercially valueless under Customs control, as the Customs authorities may decide. Such abandonment or destruction shall not entail any cost to the Revenue.

Any waste or scrap remaining after destruction shall be liable, if taken into home use, to the import duties and taxes that would be applicable to such waste and scrap imported in that state.

Removal from temporary store

19. Standard

Any person having the right to dispose of the goods shall be entitled to remove them from temporary store subject to compliance with the conditions and formalities in each case.

Note

The Customs authorities may require the person concerned to establish his right to dispose of the goods.

Goods not removed from temporary store

20. Standard

National legislation shall specify the procedure to be followed when goods are not removed from temporary store within the period laid down.

21. Recommended Practice

When goods not removed from temporary store are sold by the Customs, the proceeds of the sale, after deduction of the import duties and taxes and all other charges and expenses incurred, should either be made over to the person(s) entitled to receive them, when this is possible, or be held at their disposal for a specific period.

Information concerning temporary storage

22. Standard

The Customs authorities shall ensure that all relevant information regarding the temporary storage of goods is readily available to any person Interested.

Introduction

Goods which are imported outright for use or consumption within the Customs territory must be declared for home use.

They may be declared for home use either directly on importation or after another Customs procedure such as warehousing, temporary admission or Customs transit.

The main obligations to be fulfilled by the declarant to obtain the clearance of goods for home use are the lodgement of a Goods declaration with supporting documents (import licence, certificates of origin, etc.) and the payment of any import duties and taxes chargeable. Under certain conditions the payment of import duties and taxes may be deferred. Where appropriate, security may be required by the Customs to guarantee payment of the import duties and taxes.

The measures taken by the Customs in connexion with clearance are: checking of the Goods declaration and accompanying documents, examination of the goods, assessment and collection of import duties and taxes and release of the goods. Depending upon national administrative practice, these operations may be carried out in a different order from that shown above. The Customs may also be responsible for obtaining the data required for trade statistics and for the enforcement of other statutory or regulatory provisions relating to the control of imported goods. Other competent authorities may also carry out certain controls (veterinary, health phytopathological, etc.) on goods declared for home use.

The provisions of this Annex apply to the various formalities and measures (Customs formalities) involved in the clearance of goods for home use, whatever their mode of importation.

The Annex does not apply to the clearance for home use of goods imported by post or carried in travellers' baggage.

Definitions

For the purposes of this Annex:

(a) the term "clearance for home use" means the Customs procedure which provides that imported goods may remain permanently in the Customs territory. This procedure implies the payment of any import duties and taxes chargeable and the accomplishment of all the necessary Customs formalities;

(b) the term "import duties and taxes" means Customs duties and all other duties, taxes, fees or other charges which are collected on or in connexion with the importation of goods, but not including fees and charges which are limited in amount to the approximate cost of services rendered;

(c) the term "Goods declaration" means a statement made in the form prescribed by the Customs, by which the persons interested indicate the Customs procedure to be applied to the goods and furnish the particulars which the Customs require to be declared for the application of that procedure;

(d) the term "declarant" means the person who signs a Goods declaration or in whose name it is signed;

(e) the term "checking of the Goods declaration" means the action taken by the Customs to satisfy themselves that the Goods declaration is properly made out, that the supporting documents required are attached and that they fulfil the conditions laid down as to their authenticity and validity;

(f) the term "examination of goods" means the physical inspection of goods by the Customs to satisfy themselves that the nature, origin, condition, quantity and value of the goods are in accordance with the particulars furnished in the Goods declaration;

(g) the term "assessment of import duties and taxes" means the determination of the amount of import duties and taxes payable;

(h) the term "release" means the action by the Customs to permit goods undergoing clearance to be placed at the disposal of the persons concerned;

(ij) the term "security" means that which ensures to the satisfaction of the Customs that an obligation to the Customs will be fulfilled. Security is described as "general" when it ensures that the obligations arising from several operations will be fulfilled;

(k) the term "person" means both natural and legal persons, unless the context otherwise requires.

Principles

1. Standard

Clearance for home use shall be governed by the provisions of this Annex.

2. Standard

National legislation shall specify the conditions to be fulfilled and the Customs formalities to be accomplished for the clearance of goods for home use.

Notes

1. National legislation may include prohibitions and restrictions in respect of the importation of certain categories of goods.

2. The obligations to be fulfilled to effect the clearance of goods for home use include the lodgement of a Goods declaration, the production of supporting documents and the payment of any import duties and taxes chargeable.

Competent Customs offices

3. Standard

The Customs authorities shall designate the Customs offices at which goods may be cleared for home use. In determining the competence of these offices and their hours of business the factors to be taken into account shall include the particular requirements of trade and industry.

Notes

1. The Customs authorities may allow goods to be cleared for home use at inland Customs offices.

2. The competence of certain Customs offices may be restricted in terms of the mode of transport used or to specified categories of goods or to goods consigned to a specified region (e.g. the frontier zone or an industrial zone).

3. The Customs authorities may require that certain categories of goods (e.g., diamonds, antiques, works of art) be cleared for home use at Customs offices designated for that purpose.

4. Recommended Practice

Where corresponding Customs offices are located on a common frontier, the Customs authorities of the two countries concerned should, as far as possible, correlate the business hours and the competence of those offices.

The declarant

(a) Persons entitled to act as declarant

5. Standard

National legislation shall specify the conditions under which a person is entitled to act as declarant.

Note

The declarant need not be the owner of the goods; he may be, for example, the carrier, the forwarding agent, the consignee or an agent approved by the Customs.

6. Recommended Practice

Any person having the right to dispose of the goods should be entitled to act as declarant.

Note

The Customs authorities may require the declarant to establish his right to dispose of the goods.

(b) Responsibilities of the declarant

7. Standard

The declarant shall be held responsible to the Customs authorities for the accuracy of the particulars given in the Goods declaration and payment of the import duties and taxes.

(c) Rights of the declarant

8. Standard

Before lodging the Goods declaration the declarant shall be authorized, under such conditions as may be laid down by the Customs authorities:

(a) to inspect the goods and

(b) to draw samples.

9. Recommended Practice

The Customs authorities should not require a separate Goods declaration for home use in respect of samples allowed to be drawn under Customs supervision, provided that such samples are included in the Goods declaration for home use concerning the relevant consignment and that this declaration is lodged within the prescribed time limit.

10. Recommended Practice

In cases of special difficulty, and if so requested by the declarant, the Customs authorities should provide any necessary information available to them to assist him in completing the Goods declaration for home use.

The Goods declaration for home use

(a) Goods declaration form and contents

11. Standard

Forms for the Goods declaration for home use shall conform to the official model laid down by the competent authorities.

The competent authorities shall require the Goods declaration to provide only such particulars as are deemed necessary for the assessment and collection of import duties and taxes, the compilation of statistics and the application of the other laws and regulations which the Customs are responsible for enforcing.

Notes

1. The Customs authorities generally require:

(a) particulars relating to persons

— name and address of declarant

— name and address of importer

— name and address of consignor

(b) particulars relating to transport

— mode of transport

— identification of means of transport

(c) particulars relating to the goods

— country whence consigned and country of origin

— description of the packages (number, nature, marks and numbers, weight)

— tariff description of the goods

(d) particulars for the assessment of import duties and taxes (for each description of goods)

— tariff heading

— rates of import duties and taxes

— gross weight, net weight or other quantity

— dutiable value

(e) other particulars

— statistical item number applicable to each description of goods

— area whence the goods were consigned or reference to applicable legal provisions (where preferential treatment is claimed)

— reference to documents submitted in support of the Goods declaration

(f) place, date and signature of the declarant.

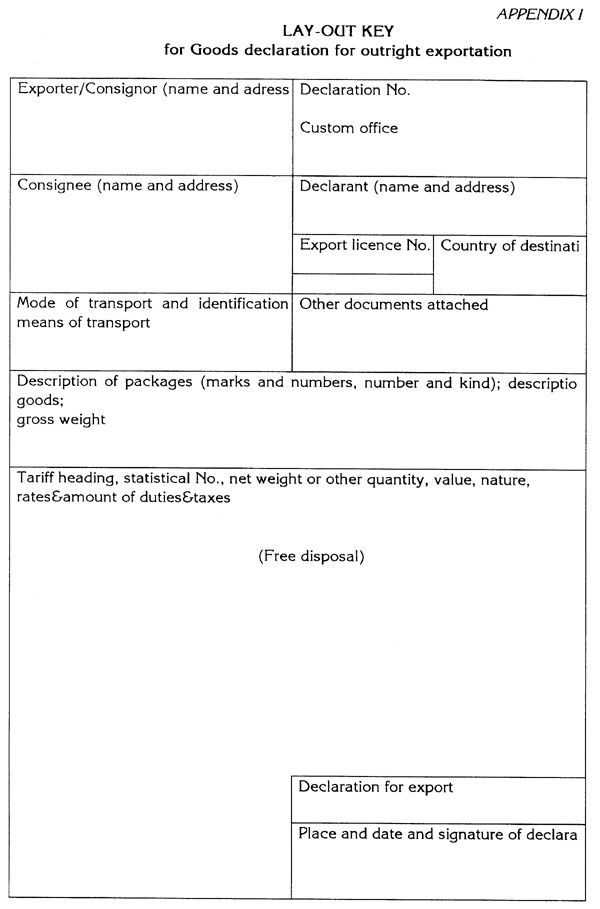

2. When they are considering revision of present forms or preparation of new forms for Goods declarations for home use, Contracting Parties may use the lay-out key in Appendix I to this Annex, having regard to the Notes in Appendix 11.

12. Recommended Practice

Where, for reasons deemed valid by the Customs authorities, the declarant does not have all the information required to make the Goods declaration for home use, he should be allowed to lodge a provisional or incomplete declaration provided that it contains the particulars deemed necessary by the Customs and that he undertakes to complete it within a specified period.

If the Customs authorities accept a provisional or incomplete declaration, the tariff treatment to be accorded to the goods should not be different from that which would have been accorded had a complete and correct declaration been lodged in the first instance.

Note

Where release is granted before all the necessary particulars have been supplied, the declarant may be required to furnish security for the payment of any sums that may become chargeable.

(b) Number of copies to be submitted

13. Recommended Practice

The Customs authorities should reduce, so far as possible, the number of copies of the Goods declaration for home use required to be submitted by the declarant.

14. Recommended Practice

Where several copies of the Goods declaration for home use are required, it should be made possible for the declarant to complete all of them in one run.

(c) Documents to be submitted in support of the Goods declaration

15. Standard

In support of the Goods declaration the Customs authorities shall require only those documents considered necessary by them in order to permit control of the operation and ensure that all requirements relating to the application of relevant restrictions or other regulations have been complied with.

Note

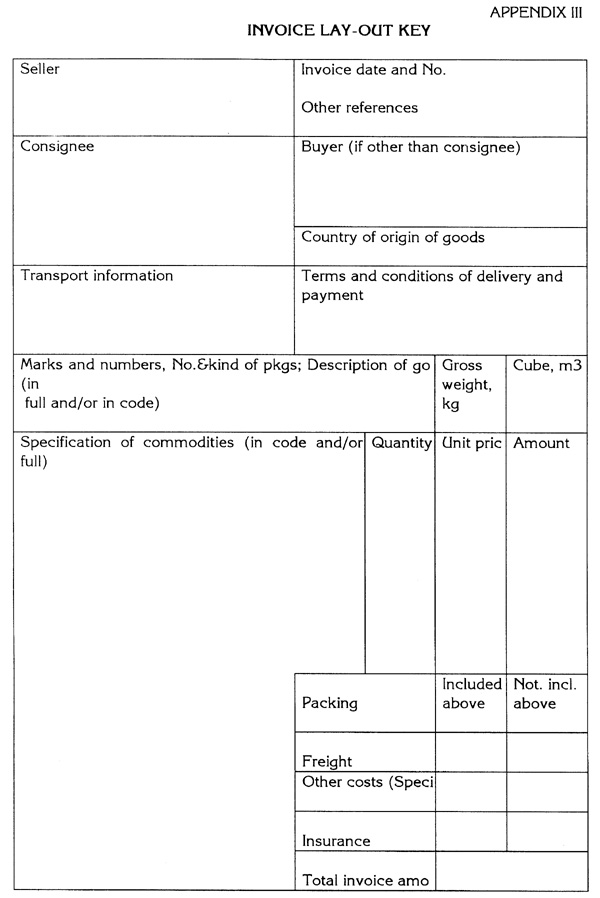

The Customs authorities frequently require production of the following documents in support of the Goods declaration for home use: import licence, documentary evidence of origin, health or phytopathological certificate, commercial invoice, transport documents.

16. Recommended Practice

Where certain supporting documents cannot be lodged with the Goods declaration and the declarant gives reasons deemed valid by the Customs authorities, the latter should authorize him to produce those documents within a specified period.

Note

Where release is granted before the missing documents are produced, the declarant may be required to furnish security for the payment of any sums that may become chargeable.

17. Recommended Practice

Where the documents produced in support of a Goods declaration are made out in a language that is not a language of the country of importation, the Customs authorities should not require, as a matter of course, a translation of the particulars given in those documents.

(d) Amendment of the Goods declaration

18. Standard

The Customs authorities shall permit the declarant to amend a Goods declaration already lodged, provided that when his request is received they have commenced neither the checking of the declaration nor the examination of the goods.

19. Recommended Practice

A request to amend a Goods declaration, submitted by the declarant after either the checking of the declaration or the examination of the goods has commenced, should be accepted by the Customs authorities if the reasons given by the declarant are deemed valid.

Note

Amendment of the Goods declaration for home use does not prevent the Customs authorities from taking any necessary action if an offence has been discovered during the checking of the declaration or the examination of the goods.

(e) Withdrawal of the Goods declaration

20. Recommended Practice

The declarant should be authorized to withdraw a Goods declaration for home use and request the application of another Customs procedure, provided that his request is made to the Customs authorities before the goods have been released and his reasons are deemed valid.

Note

Withdrawal of the Goods declaration for home use does not prevent the Customs authorities from taking any necessary action if an offence has been discovered during the checking of the declaration or the examination of the goods.

Lodgement of the Goods declaration

(a) Choice of the office of clearance

21. Standard

The Goods declaration for home use shall be lodged at the competent Customs office where the goods are presented.

Note

If standing authority has been given for the release of goods before presentation of a Goods declaration, the Customs authorities may require the Goods declaration to be lodged at a specified Customs office.

(b) Time allowed for lodgement of the declaration

22. Standard

Where national legislation lays down a time limit for lodgement of the Goods declaration for home use at a competent Customs office, the time allowed shall enable the declarant to assemble the particulars needed for making the declaration and to obtain the supporting documents required.

Notes

1. National legislation may provide that the time limits for lodgement of the Goods declaration shall run, for example, from the time when the goods are unloaded, from the time when they are presented at the Customs office or from the time when they are released.

2. When the Goods declaration has not been lodged on expiry of the time limit, the Customs authorities may take such action as may be deemed necessary, in particular to protect the interests of the Revenue.

23. Recommended Practice

At the request of the declarant, and for reasons deemed valid by the Customs authorities, the latter should extend a time limit prescribed for lodging the Goods declaration.

24. Recommended Practice

The declarant should be authorized to lodge a Goods declaration for home use at a competent Customs office before the goods arrive at that office.

Note

Authority may also be given for lodgement of the declaration before the goods arrive in the Customs territory.

(c) Periodic lodgement of declarations

25. Recommended Practice

Where goods are imported frequently by the same person, the Customs authorities should allow a single Goods declaration to cover all importations by that person in a given period.

Notes

1. The Customs authorities may make this facility subject to the condition that the importer keeps proper commercial records (e.g., by means of computers) and that the necessary control measures can be taken.

2. If the Customs authorities grant this facility, they may require the declarant to produce, at each importation, a commercial or official document (commercial invoice waybill, despatch note, etc.) giving the main particulars of the consignment concerned.

(d) Lodgement of the Goods declaration outside the business hours of the Customs office

26. Standard

The Goods declaration shall be lodged during the business hours of the competent Customs office.

27. Recommended Practice

At the request of the declarant, and for reasons deemed valid by the Customs authorities, the latter should, so far as possible, allow the Goods declaration to be lodged outside the business hours of the competent Customs office; any expenses which this entails may be charged to the declarant.

Acceptance of the Goods declaration

28. Standard

A Goods declaration shall be taken to be accepted when the Customs office at which it was lodged has ascertained that it contains all the necessary particulars and is accompanied by all the documents required.

29. Standard

Where the Customs authorities cannot accept a Goods declaration for home use lodged at a Customs office, they shall state the reasons to the declarant.

Note

A Goods declaration may be refused, for example, when the Customs office does not have the necessary competence or when the immediate production of missing documents is deemed essential.

Checking of the Goods declaration

30. Standard

The checking of the Goods declaration shall be effected as soon as possible after the declaration has been accepted.

31. Standard

For the purpose of checking the Goods declaration the Customs authorities shall take only such action as they deem essential to ensure compliance with the laws and regulations which the Customs are responsible for enforcing.

Note

As a general rule, the Customs:

— satisfy themselves that the tariff heading shown corresponds to the description of the goods and that the rates of import duties and taxes indicated are those in force;

— check that the particulars in the Goods declaration tally with those in the documents produced, in particular as regards identification of the packages and the quantity and value of the goods declared;

— check the authenticity and validity of the documents produced in support of the declaration.

Examination of the goods

(a) Time required for examination of goods

32. Standard

Where the Customs authorities decide that goods declared for home use shall be examined this examination shall take place as soon as possible after the Goods declaration has been accepted.

33. Recommended Practice

Priority should be given to the examination of live animals, perishable goods and other urgent consignments.

34. Recommended Practice

If the goods must also be inspected by other competent authorities (for the purpose of applying veterinary, health, phytopathological, etc., controls) the Customs should where practicable, perform their examination at the same time.

Note

The Customs authorities may require that goods to be examined by other competent authorities be declared at Customs offices designated for that purpose.

(b) Examination of goods outside the business hours of the Customs office

35. Standard

At the request of the declarant, and for reasons deemed valid by the Customs authorities, the latter shall, so far as possible allow goods declared for home use to be examined outside the business hours of the Customs office; the expenses entailed by such examination may be charged to the declarant.

Note

Examination outside the business hours of the Customs office may be arranged for e.g. perishable goods, live animals and other urgent consignments.

(c) Examination of goods at a place other than the Customs office

36. Standard

At the request of the declarant, and for reasons deemed valid by the Customs authorities, the latter shall, so far as possible, allow goods declared for home use to be examined at a place other than the Customs office where the Goods declaration was lodged; the expenses entailed by such examination may be charged to the declarant.

Notes

1. Goods may be examined, according to the circumstances, at the premises of the person concerned, on premises with appropriate equipment, at any place within the Customs surveillance zone or at a Customs office other than that at which the Goods declaration was lodged.

2. The cases in which arrangements may be made for examination at a place other than the Customs office where the Goods declaration was lodged include:

— goods which cannot readily be examined until unloaded at destination (for example: wheat, oil or ores imported by ship or barge; bulk consignments of parts in containers, furniture and household effects imported on transfer of residence);

— goods which cannot be examined without appropriate equipment (such as a dark room or a cold chamber);

— goods which cannot usefully be required to be produced at a Customs office (for example, products obtained from the working of border lands or quarries near the frontier, imported by the shortest route).

(d) Presence of the declarant at examination of goods

37. Standard

The declarant shall have the right to attend or to be represented at the examination of the goods. If the Customs authorities deem it useful, they may require him to be present or to be represented at the examination of the goods in order that he may give the Customs any assistance necessary to facilitate the examination.

Notes

1. The declarant may be required to group the packages, open them, sort the goods by description and tally them.

2. If goods declared for home use are dangerous, delicate or fragile, the declarant may be required to provide experts to assist the Customs.

3. The declarant may also be required to furnish the Customs with the technical specifications of imported goods.

(e) Extent of examination of goods

38. Standard

When examining goods, the Customs authorities shall take only such action as they deem essential to ensure compliance with the laws and regulations which the Customs are responsible for enforcing.

Notes

1. The examination of goods may be either summary or detailed. In a summary examination the Customs may carry out some though not necessarily all, of the following checks—counting the packages, noting their marks and numbers and ascertaining the description of the goods. Detailed examination involves thorough inspection of the goods to determine as accurately as possible their composition, quantity, tariff heading, value and, where necessary, origin.

2. Detailed examination of the goods is warranted, in particular, where the Customs authorities are not satisfied about the accuracy of particulars furnished in the declaration or in the supporting documents.

3. Goods liable to high import duties and/or taxes may be regularly subjected to detailed examination.

39. Recommended Practice

The Customs authorities should in as many cases as possible be content with a summary examination of goods declared for home use.

Note

Summary examination may be considered sufficient, for example, where goods of the same description are imported frequently by a person known by the Customs to be reliable where the accuracy of the particulars given in the declaration can be checked against the supporting documents or against other evidence, or where the import duties and taxes involved are low.

40. Recommended Practice

Where the Customs authorities carry out a detailed examination of goods shown in a declaration relating to a consignment consisting of many packages and covered by a packing list or other similar document, such examination should normally be undertaken on a random basis.

Note

The Customs authorities may decide having regard to the staff available, that consignments of goods declared for home use will be subjected to detailed examination by a selective technique.

(f) Sampling by the Customs

41.Standard

Samples shall be taken only where deemed necessary by the Customs authorities to establish the description and/or value of goods declared for home use or to ensure the application of other provisions of national legislation. Any samples drawn shall be as small as possible.

Errors in the declaration

42. Standard

If the Customs authorities find that errors in the Goods declaration or in the assessment of the import duties and taxes will cause or have caused the collection of an amount of import duties and taxes greater than that legally chargeable they shall repay or remit the amount overcharged, or shall inform the declarant so that he may amend the declaration or lodge a claim for repayment or remission, as the case may be.

43. Standard

If the Customs authorities find that errors in the Goods declaration entail liability to additional import duties and taxes. the production of additional supporting documents or the application of additional laws or regulations, and there is no evidence of illegal intent, they shall inform the declarant without delay. Where they are satisfied that the errors were inadvertent and that there has not been gross negligence on the part of the declarant they shall allow him to amend his declaration and accomplish the necessary additional formalities without imposing a penalty.

44. Standard

National legislation shall provide that where errors found in the Goods declaration or in the assessment of the import duties and taxes entail either the collection of additional import duties and taxes in an amount regarded as negligible, or the refund of such an amount, the Customs shall not collect or refund that amount.

Assessment of import duties and taxes

(a) Factors to be taken into consideration

45. Standard

National legislation shall specify the factors on which the assessment of import duties and taxes is based and the conditions under which these factors are determined.

Notes

1. The factors on which the assessment of import duties and taxes is based are generally the following:

— tariff classification;

— value or quantity, according to whether the import duties and taxes applicable are ad valorem or specific;

— country of origin or country whence consigned, where liability depends upon these factors.

2. The rules for determining tariff classification, dutiable value or quantity, and origin may be set out in explanatory notes drawn up by the competent authorities.

(b) Rates of import duties and taxes applicable

46. Standard

The rates of import duties and taxes chargeable on goods taken into home use shall be set out in official tariffs which shall be given adequate publicity.

47. Standard

National legislation shall specify the point in time to be taken into consideration for the purpose of determining the rates of import duties and taxes chargeable on goods declared for home use.

Note

The point in time taken into consideration for determining the rates chargeable may be, for example, the time when the goods arrive, the time when the Goods declaration is lodged, the time when the declaration is accepted by the Customs, the time when the Import duties and taxes are paid, or the time when the goods are released.

Payment of import duties and taxes

(a) Methods of payment accepted

48. Standard

National legislation shall specify the methods that may be used to pay the import duties and taxes chargeable.

49. Recommended Practice

The Customs authorities should permit payment other than in cash.

Notes

1. Authorized methods of payment other than cash may include bank or postal cheques, payments or transfers

2. If cheques drawn on a foreign bank are accepted it may be required that the bank must have an office in the country of importation.

(b) Date and place of payment

50. Standard

The Customs authorities shall determine the date when payment of the amount of import duties and taxes chargeable is due and the place where payment must be made.

Notes

1. Import duties and taxes are normally paid at the Customs office where the Goods declaration was lodged. Payment may also be made through another agency or office designated by the Customs authorities.

2. Import duties and taxes are generally required to be paid at the time when the Goods declaration is lodged or accepted or before the goods are released. In certain circumstances, payment may be deferred.

(c) Deferred payment of import duties and taxes

51. Recommended Practice

Persons who regularly clear goods for home use should be authorized to defer payment of import duties and taxes without interest charges.

Notes

1. A person given the benefit of this facility may be required to furnish security in an amount determined by the Customs authorities.

2. Any person wishing to defer payment may be required to submit an application in writing to the Customs.

52. Recommended Practice

If security is required for deferred payment, persons who regularly clear goods for home use at different Customs offices in the Customs territory should be authorized to provide a general security.

53. Recommended Practice

The amount of the security to be provided for deferred payment should not exceed the amount of the import duties and taxes potentially chargeable in respect of the goods imported during the period for which the payment of import duties and taxes is deferred.

Note

The Customs authorities may determine the amount of the security on the basis of the amount of the import duties and taxes paid during a previous period of the same duration. In the event of changes in, for example the rates applicable or the volume of the importations, the amount of the security may be adjusted accordingly.

54. Standard

Any person required to provide security for deferred payment shall be allowed to choose whatever form of security prescribed by national legislation is most convenient to him.

55. Recommended Practice

The period for which payment of import duties and taxes can be deferred should be at least fourteen days following the date when payment of the amount of import duties and taxes chargeable is otherwise due.

Notes

1. Different periods may be fixed for each type of tax.

2. The Customs authorities may agree that the import duties and taxes in respect of imports during a given period shall be payable on a fixed date.

(d) Proof of payment

56. Standard

When the import duties and taxes have been paid a receipt constituting proof of payment shall be issued to the payer.

Note

The receipt may be given on the declarant's copy of the declaration.

(e) Period of limitation for the collection of import duties and taxes.

57. Standard

National legislation shall specify the period within which the Customs authorities may take legal action to collect import duties and taxes not paid when due.

(f) Interest on arrears

58. Standard

National legislation shall determine the rate of interest chargeable on amounts of import duties and taxes that have not been paid when due and the conditions of application of such interest.

Release of goods

59. Standard

Goods declared for home use shall be released as soon as the Customs authorities have examined them, or decided not to examine them, provided that no offence has been found and that any import duties and taxes chargeable have been paid or that appropriate action has been taken to ensure their collection.

60. Recommended Practice

If the Customs authorities are satisfied that the declarant will subsequently accomplish all the formalities in respect of clearance for home use they should release the goods, provided that the declarant produces a commercial or official document giving the main particulars of the consignment concerned and acceptable to the Customs.

Notes

1. The Customs authorities may make it a condition for release that the supporting documents deemed essential have been produced and that the controls provided for in national legislation (veterinary, health, phytopathological, etc., controls) have been carried out by the competent authorities.

2. The declarant may be required to furnish security to ensure compliance with his undertakings to the Customs.

61. Recommended Practice

When the goods cannot be examined promptly, for instance when experts have to be called in or when the goods must be analysed in specialized laboratories, and examination is possible on the basis of samples or detailed technical documentation, the Customs authorities should not wait for the examination to be completed before they release the goods.

Note

The Customs authorities may grant release on condition that security is furnished to ensure collection of any additional import duties and taxes that might become chargeable.

62. Recommended Practice

Where an offence has been discovered during the checking of the Goods declaration or the accompanying documents or during the examination of the goods, the Customs authorities should not wait for the offense to be regularized before they release the goods, provided that the declarant furnishes security to ensure collection of the additional import duties and taxes and of the penalties to which he is liable and that the goods are not liable to confiscation.

Destruction or abandonment of goods

63. Recommended Practice

On condition that no offence has been discovered during the checking of the declaration or the examination of the goods, the declarant or the person interested should not be required to pay the import duties and taxes or should be entitled to repayment thereof:

— where at his request goods that have been declared for home use but have not been released are abandoned to the Revenue or destroyed or rendered commercially valueless under Customs control, as the Customs authorities may decide. Such abandonment or destruction shall not entail any cost to the Revenue;

— where goods that have been declared for home use are destroyed or irrecoverably lost by accident or force majeure, provided that such destruction or loss Occurs before the goods are released and is duly established to the satisfaction of the Customs authorities.

Any waste or scrap remaining after destruction shall be liable, if taken into home use, to the import duties and taxes that would be applicable to such waste or scrap imported in that state.

Note

Where an offence has been discovered, the Customs authorities may allow this facility subject to payment of the penalties laid down in national legislation.

64. Recommended Practice

Where the Customs authorities sell goods which have not been declared within the time allowed or could not be released although no offence has been discovered, the proceeds of the sale, after deduction of the import duties and taxes and all other charges and expenses incurred, should be made over to the person(s) entitled to receive them, when this is possible, or be held at their disposal for a specified period.

Note

This procedure may be followed, in particular, where a Goods declaration has been accepted but the declarant has been unable to pay the import duties and taxes and has not requested that the goods be assigned to another Customs procedure.

Information concerning clearance for home use

65. Standard

The Customs authorities shall ensure that all relevant information concerning the clearance for home use procedure is readily available to any person interested.

Appendix II

Notes